Friday, July 31, 2009

AIG Is Still Working It's Ponzi Scheme

The New York Times published an article yesterday that exposes a vast web of self-dealing and questionable business practices which continue to fester at AIG's insurance subsidiaries.

http://www.nytimes.com/2009/07/31/business/31aig.html?_r=3&dbk

"[State regulatory filings] show that A.I.G.’s individual insurance companies have been doing an unusual volume of business with each other for many years — investing in each other’s stocks; borrowing from each other’s investment portfolios; and guaranteeing each other’s insurance policies, even when they have lacked the means to make good."

The article goes on to quote a former chief insurance examiner for Louisiana who states: "If A.I.G.’s incoming premiums shrink, he warned, 'the whole thing’s going to collapse in on itself.'”

That, my friends, is definitionally a Ponzi scheme. It's no different than what Madoff was doing.

Nothing has been written truthfully about why the Govt did not put AIG into bankruptcy. But let's examine that. We know that $182 billion (that we know about) has been funnelled thru AIG into several banks, most notably Goldman Sachs. But we don't know how much each bank received and we don't know how that money was used. That's one of the primary reasons the Fed does not want to be subjected to the scrutiny of a public audit and Bernanke refuses to talk about that money flow, which comes from U.S. taxpayers, while he's under oath in front of Congress.

IF AIG HAD PUT INTO BANKRUPTCY, the way it should have been given its hopeless condition of insolvency, AIG's hidden financial data (aka off-balance-sheet derivatives agreements, etc) would have been exposed by legal discovery for all to see. Look at Enron as an example, we had no idea whatsoever just how fraudulent Enron's business was until everything was exposed in bankruptcy court. The numbers were staggering. AIG's balance is many multiples larger than was Enron's, so it is very safe to assume that AIG's fraudulent business deals are as well. The above NY Times article exposes some of this fraud.

To further this analysis, had AIG been put into bankruptcy, the big Wall Street firms who had their liability exposure, which was at least $10-20 billion for Goldman Sachs alone, would not have been able to access any of the funding used to keep AIG breathing - they would have had to stand in line with unsecured creditors waiting for any crumbs that might have been left on the table after the liquidation process finished and the lawyers were well-fed.

The bottom line is that AIG's financial condition gets worse every day and it should have been thrown into bankruptcy immediately when it hit the wall last year. It was not put into chapter 11/7 because then Tim Geithner and Hank Paulson would NOT have been unable to channel over $100 billion in taxpayer money to the Wall Street firms who made failed business bets on AIG.

http://www.nytimes.com/2009/07/31/business/31aig.html?_r=3&dbk

"[State regulatory filings] show that A.I.G.’s individual insurance companies have been doing an unusual volume of business with each other for many years — investing in each other’s stocks; borrowing from each other’s investment portfolios; and guaranteeing each other’s insurance policies, even when they have lacked the means to make good."

The article goes on to quote a former chief insurance examiner for Louisiana who states: "If A.I.G.’s incoming premiums shrink, he warned, 'the whole thing’s going to collapse in on itself.'”

That, my friends, is definitionally a Ponzi scheme. It's no different than what Madoff was doing.

Nothing has been written truthfully about why the Govt did not put AIG into bankruptcy. But let's examine that. We know that $182 billion (that we know about) has been funnelled thru AIG into several banks, most notably Goldman Sachs. But we don't know how much each bank received and we don't know how that money was used. That's one of the primary reasons the Fed does not want to be subjected to the scrutiny of a public audit and Bernanke refuses to talk about that money flow, which comes from U.S. taxpayers, while he's under oath in front of Congress.

IF AIG HAD PUT INTO BANKRUPTCY, the way it should have been given its hopeless condition of insolvency, AIG's hidden financial data (aka off-balance-sheet derivatives agreements, etc) would have been exposed by legal discovery for all to see. Look at Enron as an example, we had no idea whatsoever just how fraudulent Enron's business was until everything was exposed in bankruptcy court. The numbers were staggering. AIG's balance is many multiples larger than was Enron's, so it is very safe to assume that AIG's fraudulent business deals are as well. The above NY Times article exposes some of this fraud.

To further this analysis, had AIG been put into bankruptcy, the big Wall Street firms who had their liability exposure, which was at least $10-20 billion for Goldman Sachs alone, would not have been able to access any of the funding used to keep AIG breathing - they would have had to stand in line with unsecured creditors waiting for any crumbs that might have been left on the table after the liquidation process finished and the lawyers were well-fed.

The bottom line is that AIG's financial condition gets worse every day and it should have been thrown into bankruptcy immediately when it hit the wall last year. It was not put into chapter 11/7 because then Tim Geithner and Hank Paulson would NOT have been unable to channel over $100 billion in taxpayer money to the Wall Street firms who made failed business bets on AIG.

The Tech-Heavy Nasdaq Is Up 13.2% Since July 9th?

I preface this commentary by saying that the Nasdaq has a higher beta than the SPX or the Dow. That is, the Nasdaq will tend to make bigger percentage moves up and down for every 1% move in the SPX or the Dow. Having said that, it seems that lately the action in the whole stock market, up and down, is being led by the action in the Nasdaq. If you look at the employment data in the article I link, it would suggest that it's time to take any gains clawed back in your portfolio since the March '09 bottom and thank the Fed for that gift. The fundamantals will soon take that gift away and turn it into bigger losses:

As per the chart in the linked post at clusterstock.com, unemployment in the Silicon Valley has spiked up to 12%, which is above the statewide jobless number in California and quite a bit above the jobless number for the country as a whole (I'm using the Government-produced/manipulated number for purposes of comparison - I'm not endorsing the Govt number as being even remotely close to accurate - real unemployment is much higher).

It would seem to me that the big rally in the Nasdaq is not supported in any way by fundamental factors, other than maybe all of the money being injected in the system by the Fed. Here's the link:

http://www.businessinsider.com/henry-blodget-silicon-valley-unemployment-skyrockets-to-12-2009-7

It would also seem to me that anyone with money invested in technology or Nasdaq stocks should think about selling.

As per the chart in the linked post at clusterstock.com, unemployment in the Silicon Valley has spiked up to 12%, which is above the statewide jobless number in California and quite a bit above the jobless number for the country as a whole (I'm using the Government-produced/manipulated number for purposes of comparison - I'm not endorsing the Govt number as being even remotely close to accurate - real unemployment is much higher).

It would seem to me that the big rally in the Nasdaq is not supported in any way by fundamental factors, other than maybe all of the money being injected in the system by the Fed. Here's the link:

http://www.businessinsider.com/henry-blodget-silicon-valley-unemployment-skyrockets-to-12-2009-7

It would also seem to me that anyone with money invested in technology or Nasdaq stocks should think about selling.

Thursday, July 30, 2009

CNBC viewership down 28%

I said back in 2002 that the stock market won't reach an ultimate bottom until CNBC is out of business and off the air. We are about 28% of the way there:

http://www.zerohedge.com/article/cnbc-viewership-down-28

http://www.zerohedge.com/article/cnbc-viewership-down-28

Got Gold?

My friend "Andy in Denver" wrote the following commentary, which he generously allowed me post so that I didn't have reinvent the wheel writing the same type of commentary. In the first part, he is referring to the fact that gold production in one of the world's biggest gold mining countries - S. Africa - is plummeting with no turnaround in sight. In fact, gold production is plummeting globally and has been for the last 3 years. And this is in the context of rapidly increasing demand for the yellow dog AND rapidly declining Central Bank supply. THAT's the Golden Truth. So without further adieu:

Several very important things:

Until gold surges toward $1,500/oz, in my view, there is not a chance that this trend will be reversed, and mine production will continue to fall while demand continues to surge.

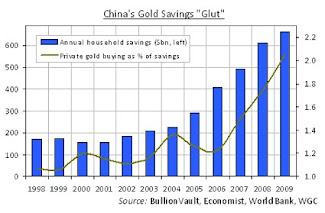

And oh yeah, the world’s Central Banks are no longer selling gold, and in fact are buyers such as the Chinese that two months ago stated that they have accumulated an additional 400 tonnes under the radar (and I guarantee they are still buying hand over fist today).

http://af.reuters.com/article/investingNews/idAFJOE56S0CJ20090729?feedType=RSS&feedName=investingNews

http://www.theaustralian.news.com.au/business/story/0,,25389227-5017999,00.html?from=public_rss

In another topic, as you know I have been persistently writing over the years that I strongly believe the gold ETFs GLD and IAU and the silver ETF SLV are potentially fraudulent, created by the gold/silver Cartel as Ponzi schemes to keep the public out of the physical gold and silver markets and as a tool (via surreptitious leasing/shorting) to suppress the gold and silver prices further. Granted, James Turk gets the blue ribbon for reporting this potential first (back when they were launched in 2004/05), but I have been very vocal about this topic ever since.

Well now it seems that we have some company, not just regarding the potentially fraudulent nature of these securities, but about the entire gold/silver futures market as well. Literally dozens of articles are being published monthly now about these topics, as the blatancy of the Cartel has gone off the charts (such as this week) in their efforts to “save the dollar”, or more likely “save the status quo” of greedy politicians and bankers such as Goldman Sachs ruling the U.S. and fleecing the public.

The below two articles, particularly the first one, give detailed evidence about the frailties of these ETFs, and anyone reading them should recognize, RIGHT AWAY, that Enron and Bernie Madoff had many of the same red flags.

http://www.zerohedge.com/article/project-mayhem-research-multiple-anomalies-detected-silver-etfs

http://seekingalpha.com/article/149209-are-gld-and-slv-legitimate-investment-vehicles

Thus, BEWARE of GLD, IAU, SLV, at all costs. Sell them immediately if you still own them.

And, on that topic, I am proud to announce that Silver Bullion Trust yesterday was priced by the same people that brought the market CEF (Central Fund of Canada, 60% gold/40% silver) and GTU (Central Gold Trust, 100% gold). Right now, it is only trading in Canada under the tickers T.SBT.U (Can $) and T.SBT.UN ($USD), but once it gets larger in size ($75 million of assets versus the current $26 million), it too, will be listed on the AMEX in the U.S..

Hands down, [because these 3 funds require actual physical audits of their gold/silver holdings] CEF/GTU/SBT are the best ways to invest in “paper gold and silver”, the antithesis of Hands down, CEF/GTU/SBT are the best ways to invest in “paper gold and silver”, the antithesis of what GLD/IAU/SLV represent [these 3 funds DO NOT permit an actual independent hands-on audit of their supposed holdings].

And finally, I needed to note that, in my view, the financial system is only worsening, not improving as stock market is trying to suggest. This week, the U.S. has had two of the worst Treasury auctions in its history (with a third coming today), and 150 Chinese diplomats are in town reading the U.S. government the riot act as it prepares to transition the world off the U.S. dollar reserve standard, which will inevitably cause accelerating inflation in the U.S. (that, coupled with the exponentially increase in printed dollars).

Predictably, of course, the gold price was hit in the U.S. futures market to try and divert attention from the weak Treasury auction and ramifications of the Chinese demands, but all they have done is make the MASSIVE reverse head and shoulders formation that much stronger.

Gold and silver WILL be breaking out sometime in the near-future, that is a foregone conclusion. And when they do, the commencement of the perception of accelerating (and potentially hyper-) inflation in the U.S. will have occurred.

Several very important things:

To start, the article below shows how the big South African gold miners are getting crushed by the big surge in the South African Rand versus the dollar, as their costs in local dollars are rising faster than the gold price, which continues to be suppressed by the gold cartel (this goes for Canadian miners as well, by the way).

http://www.miningweekly.com/article/stronger-rand-to-hit-sa-gold-producers-profits-2009-07-29

Upon returning from South Africa in February with the Rand/Dollar ratio at 10 : 1, I promptly wrote an article stating my belief that the South African Rand (due to its huge gold reserves and cheap cost of living) was the cheapest currency on the planet, and would dramatically appreciate in the next 3-5 years, likely PAST PARTITY (1 : 1).

As of today, the exchange rate has risen to roughly 7.8 : 1, yet per the article the major minors are reporting losses and/or huge reductions in profits, coupled with mine closures and layoffs that have caused South African gold production to plummet for years.

Until gold surges toward $1,500/oz, in my view, there is not a chance that this trend will be reversed, and mine production will continue to fall while demand continues to surge.

And oh yeah, the world’s Central Banks are no longer selling gold, and in fact are buyers such as the Chinese that two months ago stated that they have accumulated an additional 400 tonnes under the radar (and I guarantee they are still buying hand over fist today).

http://af.reuters.com/article/investingNews/idAFJOE56S0CJ20090729?feedType=RSS&feedName=investingNews

http://www.theaustralian.news.com.au/business/story/0,,25389227-5017999,00.html?from=public_rss

In another topic, as you know I have been persistently writing over the years that I strongly believe the gold ETFs GLD and IAU and the silver ETF SLV are potentially fraudulent, created by the gold/silver Cartel as Ponzi schemes to keep the public out of the physical gold and silver markets and as a tool (via surreptitious leasing/shorting) to suppress the gold and silver prices further. Granted, James Turk gets the blue ribbon for reporting this potential first (back when they were launched in 2004/05), but I have been very vocal about this topic ever since.

Well now it seems that we have some company, not just regarding the potentially fraudulent nature of these securities, but about the entire gold/silver futures market as well. Literally dozens of articles are being published monthly now about these topics, as the blatancy of the Cartel has gone off the charts (such as this week) in their efforts to “save the dollar”, or more likely “save the status quo” of greedy politicians and bankers such as Goldman Sachs ruling the U.S. and fleecing the public.

The below two articles, particularly the first one, give detailed evidence about the frailties of these ETFs, and anyone reading them should recognize, RIGHT AWAY, that Enron and Bernie Madoff had many of the same red flags.

http://www.zerohedge.com/article/project-mayhem-research-multiple-anomalies-detected-silver-etfs

http://seekingalpha.com/article/149209-are-gld-and-slv-legitimate-investment-vehicles

Thus, BEWARE of GLD, IAU, SLV, at all costs. Sell them immediately if you still own them.

And, on that topic, I am proud to announce that Silver Bullion Trust yesterday was priced by the same people that brought the market CEF (Central Fund of Canada, 60% gold/40% silver) and GTU (Central Gold Trust, 100% gold). Right now, it is only trading in Canada under the tickers T.SBT.U (Can $) and T.SBT.UN ($USD), but once it gets larger in size ($75 million of assets versus the current $26 million), it too, will be listed on the AMEX in the U.S..

Hands down, [because these 3 funds require actual physical audits of their gold/silver holdings] CEF/GTU/SBT are the best ways to invest in “paper gold and silver”, the antithesis of Hands down, CEF/GTU/SBT are the best ways to invest in “paper gold and silver”, the antithesis of what GLD/IAU/SLV represent [these 3 funds DO NOT permit an actual independent hands-on audit of their supposed holdings].

And finally, I needed to note that, in my view, the financial system is only worsening, not improving as stock market is trying to suggest. This week, the U.S. has had two of the worst Treasury auctions in its history (with a third coming today), and 150 Chinese diplomats are in town reading the U.S. government the riot act as it prepares to transition the world off the U.S. dollar reserve standard, which will inevitably cause accelerating inflation in the U.S. (that, coupled with the exponentially increase in printed dollars).

Predictably, of course, the gold price was hit in the U.S. futures market to try and divert attention from the weak Treasury auction and ramifications of the Chinese demands, but all they have done is make the MASSIVE reverse head and shoulders formation that much stronger.

Gold and silver WILL be breaking out sometime in the near-future, that is a foregone conclusion. And when they do, the commencement of the perception of accelerating (and potentially hyper-) inflation in the U.S. will have occurred.

Wednesday, July 29, 2009

Foreclosures Hit Record Levels in June...

adding more evidence to my post earlier this week that we will soon be entering a period of a massive bulging in bank-owned homes, the majority of which will be the larger, more expensive and harder to sell McMansions:

"prime jumbo mortgages continue to fare the worst, comparatively: foreclosures among good-credit borrowers with high loan balances are up a whopping 580% since Jan. 2008, LPS said."

The national foreclosure inventory rate was 2.86%, up from 2.5% last month, and up a whopping 86.1% from last June. It is becoming more clear that the trend in troubled prime mortgages is getting worse. Here is a link to the article:

http://www.housingwire.com/2009/07/29/report-foreclosure-inventory-hits-record-level-in-june/

Please note that, in an attempt to find a possible green shoot in the housing market, the authors of this article have borrowed a high-powered microscope with which to examine the cesspool and have decided that a one-month data sample showing that fewer borrowers appear to be going delinquent on their mortgages. Don't be fooled: that's not a green shoot - it's not even a speck of algae.

I know for a fact that banks are giving delinquent borrowers a lot more time to "cure" their delinquency because 1) the foreclosure processing pipeline is hugely backed up AND over the short-term, it makes bank balance sheets look healthier when they report lower delinquencies, so they tend to delay declaring mortgages delinquent.

I have a friend on the east coast who knows a CPA with several previously high income clients who have lost their jobs, have not made mortgage payments for months and yet have not heard anything from their banks. Those are an example of mortgages that should be declared delinquent but have not been yet. There also have been several recent articles in the media alluding to this phenomenon of banks delaying delinquency notices.

"prime jumbo mortgages continue to fare the worst, comparatively: foreclosures among good-credit borrowers with high loan balances are up a whopping 580% since Jan. 2008, LPS said."

The national foreclosure inventory rate was 2.86%, up from 2.5% last month, and up a whopping 86.1% from last June. It is becoming more clear that the trend in troubled prime mortgages is getting worse. Here is a link to the article:

http://www.housingwire.com/2009/07/29/report-foreclosure-inventory-hits-record-level-in-june/

Please note that, in an attempt to find a possible green shoot in the housing market, the authors of this article have borrowed a high-powered microscope with which to examine the cesspool and have decided that a one-month data sample showing that fewer borrowers appear to be going delinquent on their mortgages. Don't be fooled: that's not a green shoot - it's not even a speck of algae.

I know for a fact that banks are giving delinquent borrowers a lot more time to "cure" their delinquency because 1) the foreclosure processing pipeline is hugely backed up AND over the short-term, it makes bank balance sheets look healthier when they report lower delinquencies, so they tend to delay declaring mortgages delinquent.

I have a friend on the east coast who knows a CPA with several previously high income clients who have lost their jobs, have not made mortgage payments for months and yet have not heard anything from their banks. Those are an example of mortgages that should be declared delinquent but have not been yet. There also have been several recent articles in the media alluding to this phenomenon of banks delaying delinquency notices.

William Dudley Blows Smoke and Bubbles...

Bill Dudley, former Goldman Sachs employee and now Goldman's representative as head of the NY Federal Reserve Bank (the branch of the Fed in charge of oversight of Goldman Sachs), issued a call for growth in the second half of 2009. Well, we're 28 days into the second half of 2009 and the REAL economic numbers continue to deterioriate, including the durable goods orders number released to day, which was much worse than expected. We are also seeing unemployment continuing to rise, real inflation-adjusted retail sales decline and shipping and transportation indexes tank. There are several other key measures of economic activity not reported in the press or promoted by the Government which continue to deteriorate. I would argue that we have a better chance of seeing world peace in the second half of 2009 than any signs of economic growth or even stability.

He also argues that the Fed has the "tools" to cap inflation. We would love to see these "tools." Bernanke also has alluded to these "tools" under oath in front of Congress but has yet to reveal what these "tools" would be.

Dudley says that by paying interest on the reserves banks keep at the Fed, it will help prevent the banks from unleashing all the cash the Government has given them into the system. Yet, in the same breath, he says the Fed TALF program is lowering credit spreads to consumers. So Dudley thus argues the Fed can limit inflation by preventing banks from lending into the system and yet he is promoting the Fed TALF program as making it easier for consumers to get credit. Either Dudley is speaking out of both sides of his mouth in an attempt to blow smoke up our ass, or he lacks the intelligence to realize that his highly scripted speech is full of conflicting ideas. I would argue strongly for the former.

I'm not sure what other "tools" Dudley thinks the Fed can pull out of its ass. I do know that the Fed has reported markdown losses in the several 10's of billions of dollars on the toxic assets it has been purchasing. We don't know what the Fed is paying for these assets (which are backstopped by the Treasury aka taxpayer money) and we don't know who the sellers are, but we do know that the Fed would not be able to sell these "assets" to drain even close to the amount of money from the system that it injected by buying these "assets." In fact, the Fed wouldn't be able to find any bids for most of the crap.

Before you go out and start loading up on stocks based on Dudley's speech, consider who he is, where he came from, who he represents and understand that every single member of the Federal Reserve system has been saying that the worst is over and they've contained the losses in the financial system. Don't believe them as their forecasting track record is dismal.

He also argues that the Fed has the "tools" to cap inflation. We would love to see these "tools." Bernanke also has alluded to these "tools" under oath in front of Congress but has yet to reveal what these "tools" would be.

Dudley says that by paying interest on the reserves banks keep at the Fed, it will help prevent the banks from unleashing all the cash the Government has given them into the system. Yet, in the same breath, he says the Fed TALF program is lowering credit spreads to consumers. So Dudley thus argues the Fed can limit inflation by preventing banks from lending into the system and yet he is promoting the Fed TALF program as making it easier for consumers to get credit. Either Dudley is speaking out of both sides of his mouth in an attempt to blow smoke up our ass, or he lacks the intelligence to realize that his highly scripted speech is full of conflicting ideas. I would argue strongly for the former.

I'm not sure what other "tools" Dudley thinks the Fed can pull out of its ass. I do know that the Fed has reported markdown losses in the several 10's of billions of dollars on the toxic assets it has been purchasing. We don't know what the Fed is paying for these assets (which are backstopped by the Treasury aka taxpayer money) and we don't know who the sellers are, but we do know that the Fed would not be able to sell these "assets" to drain even close to the amount of money from the system that it injected by buying these "assets." In fact, the Fed wouldn't be able to find any bids for most of the crap.

Before you go out and start loading up on stocks based on Dudley's speech, consider who he is, where he came from, who he represents and understand that every single member of the Federal Reserve system has been saying that the worst is over and they've contained the losses in the financial system. Don't believe them as their forecasting track record is dismal.

Tuesday, July 28, 2009

SLV Is Now Exposed As A Fraud

Project Mayhem Research has published a report showing several inconsistencies in the reporting of the silver that SLV is supposed to have in custody. These inconsistencies include "the presence of internal duplicates, rough internal duplicates, weight duplicates, statistical clustering, and cross-reference duplicates."

This calls into question whether or not the custodian, JP Morgan, can actually prove to the world that it has in its custody all of the silver that it is supposed to be holding in custody - that would be the silver that investors are assuming is really there when they invest in SLV as a surrogate silver investment. And those investors would include large pension and mutual funds.

The problem is that, as per the prospectus of SLV, nobody can force JP Morgan to prove that the silver is really there. There have been some ETFs recently that actually mandate in the prospectus that a physical audit of the custodian has to occur at least once a year. SIVR is the latest and it requires twice per year.

How come GLD and SLV do not mandate this? Is it any coincidence that JPM, who holds about 80% of the silver short interest on the Comex ALSO happens to be the trustee of SLV?

If you don't think there's foul play there, then you probably believe O.J. is innocent.

Greenlight Capital voted with its money and dumped its GLD holdings - it was the largest holder - and acquired physical bullion for its own safekeeping. THAT should be all you need to know...

Here is a copy of the research report, which I sourced from www.zerohedge.com:

http://www.zerohedge.com/sites/default/files/SilverETFs_1_PDF.pdf

If you own SLV, I would strongly recommend that you sell your shares and either buy physical silver coins for your own safekeeping, or invest in an ETF like SIVR, which requires that the trustee provides a physical audit of the custodian's silver holdings twice a year. To continue holding onto your SLV exposes you to the risk of being Madoff'd.

This calls into question whether or not the custodian, JP Morgan, can actually prove to the world that it has in its custody all of the silver that it is supposed to be holding in custody - that would be the silver that investors are assuming is really there when they invest in SLV as a surrogate silver investment. And those investors would include large pension and mutual funds.

The problem is that, as per the prospectus of SLV, nobody can force JP Morgan to prove that the silver is really there. There have been some ETFs recently that actually mandate in the prospectus that a physical audit of the custodian has to occur at least once a year. SIVR is the latest and it requires twice per year.

How come GLD and SLV do not mandate this? Is it any coincidence that JPM, who holds about 80% of the silver short interest on the Comex ALSO happens to be the trustee of SLV?

If you don't think there's foul play there, then you probably believe O.J. is innocent.

Greenlight Capital voted with its money and dumped its GLD holdings - it was the largest holder - and acquired physical bullion for its own safekeeping. THAT should be all you need to know...

Here is a copy of the research report, which I sourced from www.zerohedge.com:

http://www.zerohedge.com/sites/default/files/SilverETFs_1_PDF.pdf

If you own SLV, I would strongly recommend that you sell your shares and either buy physical silver coins for your own safekeeping, or invest in an ETF like SIVR, which requires that the trustee provides a physical audit of the custodian's silver holdings twice a year. To continue holding onto your SLV exposes you to the risk of being Madoff'd.

More On The TRUTH About The Housing Market

Several analysts were spinning the slight bounce in the Case-Schiller home price index today by exclaiming that today's number is a green shoot. I'd like to un-spin this by saying that I predicted in February that we might see a slight dead-cat bounce in housing this spring as the trillions being printed by the Fed and injected into the system would cause a slight pause in the downward spiral in volumn and prices.

Enjoy this bounce while it lasts. Here is a very ominous quote from Mark Hanson of

http://www.fieldcheckgroup.com/blog/

“National New Home Sales, on a monthly basis, don’t even add up to half of the total foreclosure activity in California alone in a single month.”

And that is just California's foreclosures. Add in the rest of the country and you have a recipe for a supply/demand catastrophe. The next leg down in this mess is going to hit in the next few months. Anectdotally, I know someone who put a McMansion on the market here in Denver a few months ago priced at a $1 million. They had no showings. They reduced it to $900k - no showings. They are considering pricing it down to $700,000 to see if it will move.

This was in yesterday's Chicago Tribune, which featured a house that had been originally offered at $4 million and is now priced at $2.85 million:

"Luxury prices keep falling - Mansions priced at $1 million-plus are harder to sell, so owners ask for less -- and add perks"

Enjoy this bounce while it lasts. Here is a very ominous quote from Mark Hanson of

http://www.fieldcheckgroup.com/blog/

“National New Home Sales, on a monthly basis, don’t even add up to half of the total foreclosure activity in California alone in a single month.”

And that is just California's foreclosures. Add in the rest of the country and you have a recipe for a supply/demand catastrophe. The next leg down in this mess is going to hit in the next few months. Anectdotally, I know someone who put a McMansion on the market here in Denver a few months ago priced at a $1 million. They had no showings. They reduced it to $900k - no showings. They are considering pricing it down to $700,000 to see if it will move.

This was in yesterday's Chicago Tribune, which featured a house that had been originally offered at $4 million and is now priced at $2.85 million:

"Luxury prices keep falling - Mansions priced at $1 million-plus are harder to sell, so owners ask for less -- and add perks"

Gold Attacked on Comex as August Options Expire Today

As is typical when it's options expiration day for the front-month Comex gold futures contract, the price of gold was aggressively slammed this morning with no news to explain fundamental reasons and no movement in other correlating commodities to explain technical reasons.

Based on the "structure" of the open interest in calls and puts, the big banks, who typically write/sell futures options to speculators, can maximize their profits if they can force August gold to close below $940 at the end of Comex trading today. We'll see if they can get that done.

This week is also "roll" week, in which anyone who is long August gold futures and is not going to take physical delivery has to liquidate their long position by the close of trading Thursday, which is the day before 1st notice day on Friday (1st notice day is the first day delivery notices are assigned, and those taking delivery must have their delivery pre-funded by then).

Roll week is usually a week in which it is easy for the the large Wall Street banks with big short positions in gold futures to put excessive downward pressure on the price of gold, as a lot of selling in the front-month contract occurs as speculators are forced to liquidate front-month positions.

Monday, July 27, 2009

New Home Sales Report is a Farce

The Commerce Department released new homes sales for June today and the spinmeisters on CNBC et. al. were gleefully exalting the 11% rise over in "estimated" new home sales for June. But let's examine the "caveat" footnote that accompanies the release:

"* 90% confidence interval includes zero. The Census Bureau does not have sufficient statistical evidence to conclude that the actual change is different from zero" (emphasis is mine).

This means that Government-reported number that caused the stock market to spike higher on the release may actually be a completely useless and meaningless number.

And in fact, the number estimated for June 2009 is over 21% below the number estimated number for June.

Here's the full release:

http://www.census.gov/const/newressales.pdf

Is this the kind of data you want your money manager to base your investments on? The reality is that the Government has no idea what the real number is for new home sales. Given that we know for a fact that a lot less people are employed every month and that the ability to get mortgage financing is exceedingly more difficult, especially for non-conforming mortgages over $417,000, it is safe to say that the new home sales for June was much lower than is being reported and would probably shock all of us in its paucity if we knew the truth.

"* 90% confidence interval includes zero. The Census Bureau does not have sufficient statistical evidence to conclude that the actual change is different from zero" (emphasis is mine).

This means that Government-reported number that caused the stock market to spike higher on the release may actually be a completely useless and meaningless number.

And in fact, the number estimated for June 2009 is over 21% below the number estimated number for June.

Here's the full release:

http://www.census.gov/const/newressales.pdf

Is this the kind of data you want your money manager to base your investments on? The reality is that the Government has no idea what the real number is for new home sales. Given that we know for a fact that a lot less people are employed every month and that the ability to get mortgage financing is exceedingly more difficult, especially for non-conforming mortgages over $417,000, it is safe to say that the new home sales for June was much lower than is being reported and would probably shock all of us in its paucity if we knew the truth.

Sunday, July 26, 2009

It's PRIME TIME: Stage 2 of the U.S. Collapse

To listen to our political leaders, the mainstream media and financial bubblevision t.v. programs, you would think that the financial crisis has stabilized and the housing market is bottoming. But if you un-spin the data fed to us by the Government and the media, the facts show that the financial system is on the precipice of another very large crisis. As the housing market collapse spreads into the prime-rated mortgage sector, a veritable avalanche of foreclosed middle to high-end homes will flood the market, triggering a much larger credit and economic crisis than what was experienced during the past 18 months.

The onset of the financial crisis in this country last year was largely precipitated by the inevitable bursting of the housing and mortgage bubble. In what was an unregulated multi-trillion dollar Ponzi scheme, the price of houses rose to unsustainably insane valuation levels, fueled by the reckless and tragic use of no-holds-barred mortgage financing. This "Stage 1" of the financial collapse was triggered by an escalation in defaults and foreclosures primarily in the subprime and Alt-A mortgage sectors. The associated collateral damage from this reverberated into the implosion $100's of billions of off-balance-sheet assets and derivatives, many of which were fraudulently rated by the rating agencies and recklessly pumped into investors by Wall Street. This took the Dow from 14,000 to 6,440 and was addressed by the Government/Fed with as much as $24 trillion in direct monetary injections and financial guarantees. During this Stage 1 we saw the Government takeover of Fannie Mae, Freddie Mac, the de facto Government takeover of AIG, the collapse of Bear Stearns, Lehman, Merrill Lynch, Countrywide, Washington Mutual, Wachovia; the U.S. auto industry, among many any other corporate failures and smaller regional bank collapses (64 smaller bank failures this year as of 7/24/09).

Stage 2 of the financial collapse of the U.S. is being triggered by the accelerating rates of default/foreclosure in the prime-rated mortgage market, as well as the collapse of commercial real estate. I am going to focus on the residential mortgage component, as it is three times as large as the commercial real estate mortgage market. Whereas the subprime and Alt-A mortgage markets are roughly $1.5 trillion combined, the prime-rate mortgage market is in excess of $10 trillion, depending on your source of data. For purposes of my analysis, I am using data presented by Mark Hanson of Field Check Group in his "7-19 Mortgage Default Crisis - Brutal Past Two-Months" article posted here (any housing/foreclosure data I use comes from this article):

http://www.fieldcheckgroup.com/2009/07/19/7-19-mortgage-default-crisis-brutal-past-two-months/

I have been asserting that the housing collapse would not end until prices fall enough to balance out the supply/demand equation. This includes the inventory of new and existing homes for sale, the inventory of foreclosed homes either on the market or being held by banks but not listed for sale AND the inventory of rental units. Data released this past week show that the rental unit vacancy rate surged to an all-time high. This will put downward pressure on rental rates, of which I am already seeing evidence in Denver. As rental rates decline, it becomes relatively more attractive to rent rather than to own, putting more downward pressure on the price buyers will be willing to pay to buy a home vs. rent.

The biggest problem, however, facing the housing market, is the impending surge in bank foreclosure inventory, fueled by the rapid increase in defaults and foreclosures in the $10 trillion prime mortgage sector of the market. Delinquencies surged in May and foreclosure inventories hit new highs. The May foreclosure rate hit 2.79% of all mortgages. This foreclosure rate increased from April to May by 6.2% and surged from May 2008 by 88.3%. Further troubling is the 5% spike in the rate of delinquencies from April to May. This compares to the April to May average increase in delinquencies over the past four years of 1.1%. The increase in delinquencies from May 2008 to May 2009 spiked up by 50%.

What's most troubling about this data is that the main source of these horrific foreclosure/default numbers is the rapid increase in defaults in Prime-rated mortgages over the last six months. Once a mortgage defaults, it typically takes 12 to 18 months for the property to be foreclosed and either listed for sale for held in suspense by banks hoping for a miracle in the condition of the housing market.

The default/foreclosure statistics for Prime mortgages are starting to follow the same statistical path experienced in the subprime and Alt-A markets. Currently, over 12% of all subprime mortgages and 8% of all Alt-A mortgages have been foreclosed. Let's assume that the total foreclosure rate for the prime mortgage market eventually hits 5%. I believe this is a conservative estimate given what has already occurred in subprime and Alt-A, the surging rate of delinquencies in the prime sector and the rapidly escalating rate of unemployment, which directly correlates to mortgage defaults. Assuming 5% means that $500 billion in prime mortgages will be foreclosed. This equates to the entire size of the subprime mortgage market. Imagine the damage this is going to cause to the entire financial system in this country. And my guesstimate may well be way too low (it is not too high, I can assure you of that).

To put this in perspective, Stage 1 of the financial collapse primarily affected the middle to lower income demographics who purchased a home using subprime and Alt-A financing. A lot of these properties are being purchased and turned into rentals, fueling the rental inventories. In what will be a much larger and more severe Stage 2, accelerating defaults in the prime mortgage sector will cause foreclosures to balloon in the upper-middle (think of overbuilt suburban McMansion developments or overvalued renovation homes in trendy urban areas) and high income neighborhoods. Anecdotally, as I drive through all the trendy renovated urban enclaves around Denver, I see "for sale" and "for rent" signs popping up like uncontrolled weeds as homeowners attempt to avoid foreclosure by selling or renting. It's one thing for an investor to scoop up several low-priced homes and rent them out, hoping for future price recovery. But how will the housing market ever absorb a massive increase in larger, overvalued homes which would never have been built in the first place if a housing bubble never occurred?

As this prime mortgage-financed foreclosure inventory balloons, it is going to drive prices down to levels thought unimaginable. As the value of the collateral for the mortgages declines, banks and investors who own the associated mortgage and mortgage-related paper will suffer massive hits to the value of their assets. Even worse, we will see another round of derivative-related bank and insurance company implosions, some of which will vaporize into thin air the way Bear Stearns and Lehman did, and Countrywide, Wash Mutual, Wachovia and Merrill should have, were it not for the taxpayer financed bailouts of these firms. This Stage of the financial collapse will likely bring down several large State and corporate pension plans as well.

And finally, how will the Federal Reserve and Treasury deal with this impending financial explosion? If it took $24 trillion of direct and indirect financial support and monetary printing in order to "stabilize" the shock of Stage 1, how much money-printing will it take in order to hold the system together as Stage 2 materializes and engulfs our system with multiple financial disasters? It can be argued that the collapse of CIT is the first sign of Stage 2 hitting. It will be interesting to see which other financial firms hit the wall. We know that Bank of America - which sits on Countrywide and Merrill Lynch's subprime mess, Wells Fargo - which sits perched on Wachovia's $122 billion of explosive Pay-Option ARM paper, and GE Capital - a giant-sized CIT - are prime candidates to be vaporized by their nuclear balance sheets.

To conclude, based on the spin-free data presented above, a bottom to the housing market is nowhere in sight. In fact, I would argue that housing prices have at least another 30-40% to fall from where they are now. This is a guesstimate based on all of the above evidence. I don't know what general level of valuation will mark the end of the housing market freefall. I do know that all the so-called experts (like Ben Bernanke et. al.) who said less than 18 months ago that the financial crisis would be contained to the subprime mortgage market and would top out at $200 billion were tragically wrong in their assessment. I also know that I am on record saying prices will revert to 1981 levels and that this crisis would end up costing $5-10 trillion. Looks like the jury is out on home prices and I was way too low on the dollar cost. I also know that, not only are we nowhere near a bottom, but that the worst is yet to occur.

Clearly, the above analysis means that investors should be taking advantage of this bear market stock rally to sell their stocks, sell all of their bonds except for maybe Treasury TIPS and start moving as much money as possible into physical gold, silver and mining stocks.

The onset of the financial crisis in this country last year was largely precipitated by the inevitable bursting of the housing and mortgage bubble. In what was an unregulated multi-trillion dollar Ponzi scheme, the price of houses rose to unsustainably insane valuation levels, fueled by the reckless and tragic use of no-holds-barred mortgage financing. This "Stage 1" of the financial collapse was triggered by an escalation in defaults and foreclosures primarily in the subprime and Alt-A mortgage sectors. The associated collateral damage from this reverberated into the implosion $100's of billions of off-balance-sheet assets and derivatives, many of which were fraudulently rated by the rating agencies and recklessly pumped into investors by Wall Street. This took the Dow from 14,000 to 6,440 and was addressed by the Government/Fed with as much as $24 trillion in direct monetary injections and financial guarantees. During this Stage 1 we saw the Government takeover of Fannie Mae, Freddie Mac, the de facto Government takeover of AIG, the collapse of Bear Stearns, Lehman, Merrill Lynch, Countrywide, Washington Mutual, Wachovia; the U.S. auto industry, among many any other corporate failures and smaller regional bank collapses (64 smaller bank failures this year as of 7/24/09).

Stage 2 of the financial collapse of the U.S. is being triggered by the accelerating rates of default/foreclosure in the prime-rated mortgage market, as well as the collapse of commercial real estate. I am going to focus on the residential mortgage component, as it is three times as large as the commercial real estate mortgage market. Whereas the subprime and Alt-A mortgage markets are roughly $1.5 trillion combined, the prime-rate mortgage market is in excess of $10 trillion, depending on your source of data. For purposes of my analysis, I am using data presented by Mark Hanson of Field Check Group in his "7-19 Mortgage Default Crisis - Brutal Past Two-Months" article posted here (any housing/foreclosure data I use comes from this article):

http://www.fieldcheckgroup.com/2009/07/19/7-19-mortgage-default-crisis-brutal-past-two-months/

I have been asserting that the housing collapse would not end until prices fall enough to balance out the supply/demand equation. This includes the inventory of new and existing homes for sale, the inventory of foreclosed homes either on the market or being held by banks but not listed for sale AND the inventory of rental units. Data released this past week show that the rental unit vacancy rate surged to an all-time high. This will put downward pressure on rental rates, of which I am already seeing evidence in Denver. As rental rates decline, it becomes relatively more attractive to rent rather than to own, putting more downward pressure on the price buyers will be willing to pay to buy a home vs. rent.

The biggest problem, however, facing the housing market, is the impending surge in bank foreclosure inventory, fueled by the rapid increase in defaults and foreclosures in the $10 trillion prime mortgage sector of the market. Delinquencies surged in May and foreclosure inventories hit new highs. The May foreclosure rate hit 2.79% of all mortgages. This foreclosure rate increased from April to May by 6.2% and surged from May 2008 by 88.3%. Further troubling is the 5% spike in the rate of delinquencies from April to May. This compares to the April to May average increase in delinquencies over the past four years of 1.1%. The increase in delinquencies from May 2008 to May 2009 spiked up by 50%.

What's most troubling about this data is that the main source of these horrific foreclosure/default numbers is the rapid increase in defaults in Prime-rated mortgages over the last six months. Once a mortgage defaults, it typically takes 12 to 18 months for the property to be foreclosed and either listed for sale for held in suspense by banks hoping for a miracle in the condition of the housing market.

The default/foreclosure statistics for Prime mortgages are starting to follow the same statistical path experienced in the subprime and Alt-A markets. Currently, over 12% of all subprime mortgages and 8% of all Alt-A mortgages have been foreclosed. Let's assume that the total foreclosure rate for the prime mortgage market eventually hits 5%. I believe this is a conservative estimate given what has already occurred in subprime and Alt-A, the surging rate of delinquencies in the prime sector and the rapidly escalating rate of unemployment, which directly correlates to mortgage defaults. Assuming 5% means that $500 billion in prime mortgages will be foreclosed. This equates to the entire size of the subprime mortgage market. Imagine the damage this is going to cause to the entire financial system in this country. And my guesstimate may well be way too low (it is not too high, I can assure you of that).

To put this in perspective, Stage 1 of the financial collapse primarily affected the middle to lower income demographics who purchased a home using subprime and Alt-A financing. A lot of these properties are being purchased and turned into rentals, fueling the rental inventories. In what will be a much larger and more severe Stage 2, accelerating defaults in the prime mortgage sector will cause foreclosures to balloon in the upper-middle (think of overbuilt suburban McMansion developments or overvalued renovation homes in trendy urban areas) and high income neighborhoods. Anecdotally, as I drive through all the trendy renovated urban enclaves around Denver, I see "for sale" and "for rent" signs popping up like uncontrolled weeds as homeowners attempt to avoid foreclosure by selling or renting. It's one thing for an investor to scoop up several low-priced homes and rent them out, hoping for future price recovery. But how will the housing market ever absorb a massive increase in larger, overvalued homes which would never have been built in the first place if a housing bubble never occurred?

As this prime mortgage-financed foreclosure inventory balloons, it is going to drive prices down to levels thought unimaginable. As the value of the collateral for the mortgages declines, banks and investors who own the associated mortgage and mortgage-related paper will suffer massive hits to the value of their assets. Even worse, we will see another round of derivative-related bank and insurance company implosions, some of which will vaporize into thin air the way Bear Stearns and Lehman did, and Countrywide, Wash Mutual, Wachovia and Merrill should have, were it not for the taxpayer financed bailouts of these firms. This Stage of the financial collapse will likely bring down several large State and corporate pension plans as well.

And finally, how will the Federal Reserve and Treasury deal with this impending financial explosion? If it took $24 trillion of direct and indirect financial support and monetary printing in order to "stabilize" the shock of Stage 1, how much money-printing will it take in order to hold the system together as Stage 2 materializes and engulfs our system with multiple financial disasters? It can be argued that the collapse of CIT is the first sign of Stage 2 hitting. It will be interesting to see which other financial firms hit the wall. We know that Bank of America - which sits on Countrywide and Merrill Lynch's subprime mess, Wells Fargo - which sits perched on Wachovia's $122 billion of explosive Pay-Option ARM paper, and GE Capital - a giant-sized CIT - are prime candidates to be vaporized by their nuclear balance sheets.

To conclude, based on the spin-free data presented above, a bottom to the housing market is nowhere in sight. In fact, I would argue that housing prices have at least another 30-40% to fall from where they are now. This is a guesstimate based on all of the above evidence. I don't know what general level of valuation will mark the end of the housing market freefall. I do know that all the so-called experts (like Ben Bernanke et. al.) who said less than 18 months ago that the financial crisis would be contained to the subprime mortgage market and would top out at $200 billion were tragically wrong in their assessment. I also know that I am on record saying prices will revert to 1981 levels and that this crisis would end up costing $5-10 trillion. Looks like the jury is out on home prices and I was way too low on the dollar cost. I also know that, not only are we nowhere near a bottom, but that the worst is yet to occur.

Clearly, the above analysis means that investors should be taking advantage of this bear market stock rally to sell their stocks, sell all of their bonds except for maybe Treasury TIPS and start moving as much money as possible into physical gold, silver and mining stocks.

Saturday, July 25, 2009

Capital One's (COF) Earnings Fantasy

Capitol One SHOULD HAVE reported a net LOSS of $120 million.

Capital One's stockd higher Friday after the Company released earings which were better than expected. They reported net income of $220 million, not including charges related to paying back TARP. Technically the market should care about those charges but I'll let that one slip by. MORE important, COF created their net income out of thin air by reducing their provision for loan losses. They reduced this accounting charge by $345 million from the amount they used the 1st quarter, DESPITE the fact that their total charge off rate spiked up to 9.3% in the 2nd quarter from 7.3% in the 1st quarter and from 6.07% in the 2nd quarter of 2008. If they had just held their provision for losses flat, they would have reported at net loss of $120 million (they will tell your their managed assets declined, HOWEVER, their charge-off rates more than offset this and their NET assets were basically flat, so strike that b.s. from the record).

The charge-off trend is not COF's friend. If anything, they should have INCREASED the amount they "provision" for loan losses, rather than decrease that amount, especially since they "provision" rate is about 1/2 of the actual charge-off rate. IN FACT, investors should penalize COF for not being a lot more conservative in this area of accounting. They even said in their conference call that they expect higher charge-offs in the future, so why do analysts let them get away with this crap?

In their explanation, Capital One wraps a loosely spun story around their reduction in loan loss provision for Q2. Don't believe it. If anything, analysts should be all over that - but they won't be. In another troubling trend, the default rates across all of their lending at their Chevy Chase bank subsidiary have spiked higher again. Another no-friend trend for COF. These business lines include commericial real estate, auto loans and home mortgages. And everyone knows that the charge-offs in credit cards are accelerating higher.

I would imagine that if I took the time to pour over the 10Q when they file it, I would find that is in much worse financial condition than is presented in their fictitious quarterly earnings report and I could decimate their "higher" Tangible Common Equity calculation, which they proudly strutted to analysts and I'm sure is based on more fantasy.

Capital One's stockd higher Friday after the Company released earings which were better than expected. They reported net income of $220 million, not including charges related to paying back TARP. Technically the market should care about those charges but I'll let that one slip by. MORE important, COF created their net income out of thin air by reducing their provision for loan losses. They reduced this accounting charge by $345 million from the amount they used the 1st quarter, DESPITE the fact that their total charge off rate spiked up to 9.3% in the 2nd quarter from 7.3% in the 1st quarter and from 6.07% in the 2nd quarter of 2008. If they had just held their provision for losses flat, they would have reported at net loss of $120 million (they will tell your their managed assets declined, HOWEVER, their charge-off rates more than offset this and their NET assets were basically flat, so strike that b.s. from the record).

The charge-off trend is not COF's friend. If anything, they should have INCREASED the amount they "provision" for loan losses, rather than decrease that amount, especially since they "provision" rate is about 1/2 of the actual charge-off rate. IN FACT, investors should penalize COF for not being a lot more conservative in this area of accounting. They even said in their conference call that they expect higher charge-offs in the future, so why do analysts let them get away with this crap?

In their explanation, Capital One wraps a loosely spun story around their reduction in loan loss provision for Q2. Don't believe it. If anything, analysts should be all over that - but they won't be. In another troubling trend, the default rates across all of their lending at their Chevy Chase bank subsidiary have spiked higher again. Another no-friend trend for COF. These business lines include commericial real estate, auto loans and home mortgages. And everyone knows that the charge-offs in credit cards are accelerating higher.

I would imagine that if I took the time to pour over the 10Q when they file it, I would find that is in much worse financial condition than is presented in their fictitious quarterly earnings report and I could decimate their "higher" Tangible Common Equity calculation, which they proudly strutted to analysts and I'm sure is based on more fantasy.

Housing's Endless Downward Spiral

When you strip out the unit percentage gains achieved by revising down the previous month's reported number, and take away the foreclosure/short sale volumn out of the housing numbers, you conclude that not only is the market NOT "stabilizing," but that the housing marke is still in state of freefall, albeit a freefall that is slowing down a bit (not necessarily any sign of stability, as you would expect that the rate of decline would slow down over time anyway).

What will add fuel to the decline in the value of housing is the surging number of rental units. And this is occurring despite a big shift in the market from buying to renting. As Calculated Risk reported yesterday, the rental vacancy rate is at an all-time high:

http://www.calculatedriskblog.com/2009/07/surge-in-rental-units.html

As rental vacancies surge, rents will decline and this will put further downward pressure on the price people are willing to pay to buy a home. This is a vicious downward spiral which will not stop until the supply and demand equation balances out. Right now there were just way too many housing units - both homes and apartments - that were built in the last few years and prices are way too high right now to foster any semblence of supply/demand balance.

Anectdotally speaking, at least in Denver, I'm seeing more and more "for sale" and "for rent" signs being posted all over the city, especially in areas didn't seem to have much on the market. I know the guy who owns the 3-unit townhome complex I live in and has the middle unit on the market for about 15% less than was originally being asked for a year ago as a brand new unit told me that he's had only 8 showings in 4 weeks and the only comments were that 2 of the showings inquired about renting. I live in an area that was one of the hottest markets during the bubble.

My best guess is that, overall across the country, we will see housing prices decline at least another 20-30% before we reach anything that can be considered a bottom. And that bottom could drift sideways for a very long time.

What will add fuel to the decline in the value of housing is the surging number of rental units. And this is occurring despite a big shift in the market from buying to renting. As Calculated Risk reported yesterday, the rental vacancy rate is at an all-time high:

http://www.calculatedriskblog.com/2009/07/surge-in-rental-units.html

As rental vacancies surge, rents will decline and this will put further downward pressure on the price people are willing to pay to buy a home. This is a vicious downward spiral which will not stop until the supply and demand equation balances out. Right now there were just way too many housing units - both homes and apartments - that were built in the last few years and prices are way too high right now to foster any semblence of supply/demand balance.

Anectdotally speaking, at least in Denver, I'm seeing more and more "for sale" and "for rent" signs being posted all over the city, especially in areas didn't seem to have much on the market. I know the guy who owns the 3-unit townhome complex I live in and has the middle unit on the market for about 15% less than was originally being asked for a year ago as a brand new unit told me that he's had only 8 showings in 4 weeks and the only comments were that 2 of the showings inquired about renting. I live in an area that was one of the hottest markets during the bubble.

My best guess is that, overall across the country, we will see housing prices decline at least another 20-30% before we reach anything that can be considered a bottom. And that bottom could drift sideways for a very long time.

Friday, July 24, 2009

Something To Think About

the next time you hear the dopes on CNBC or the dope in charge of the Federal Reserve say that there are signs the economy is improving:

“…there are indications that the severest phase of the recession is over…”- Harvard Economic Society (HES) Jan 18, 1930

“…there are indications that the severest phase of the recession is over…”- Harvard Economic Society (HES) Jan 18, 1930

Subscribe to:

Posts (Atom)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/sp_en_6.gif)